case study1

- Q1(Effective return)

-

- info

- Q2(Duration and convexity)

-

- info

- Q3(bootstrap and related rates)

- Q4( The minimum variance portfolios for target returns)

-

- Info

https://zhuanlan.zhihu.com/p/139262608#

利率衍生品定价的基础内容回顾

Q1(Effective return)

info

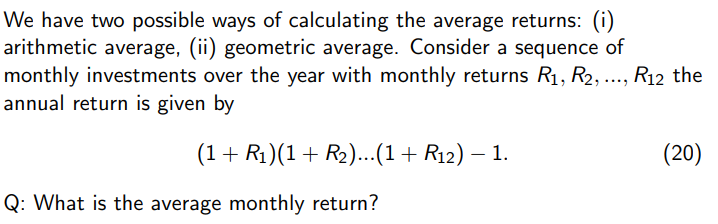

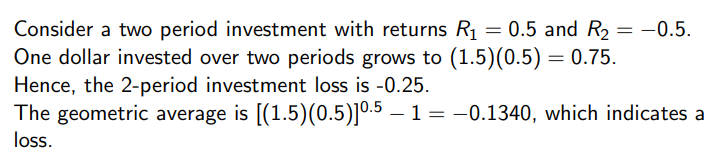

two ways to calculate the average of return

1)arithmetic average

2) geometric average

Head:

Tom and Amy both bought a 20-year pension with different return schemes. Tom’s pension has first year interest rate of 3% and will increase by 0.5% every year whilst Amy’s pension has a continuous interest rate of 7%. Both pension pays the interest annually. Compare the benefits of the two pensions by computing their effective rates of return.

%% Solution:

InterestR_Tom=[3:0.5:12.5]/100;

EffectiveR_Tom=(prod(1+[3:0.5:12.5]/100))^(1/20)-1;% 用平均来算

EffectiveR_Tom=prod(EffectiveR_AMY=exp(0.07)-1;if EffectiveR_Tom>EffectiveR_AMYdisp('The pension of Tom has higher effective rate')

elseif EffectiveR_Tom<EffectiveR_AMYdisp('The pension of Amy has higher effective rate')

elsedisp('The effective rates are equal')

endQ2(Duration and convexity)

info

wirte a user_defined matlab-code and call it

function [Price,duration,convexity] = DurationConvexity(Face,Coupon,Maturity,yield)

% BondPrice, Duration and ConvexityTime=0.5:0.5:Maturity; % time for paymentsC = 0.5*Coupon*Face; % one coupon paymentPrice = sum(C*exp(-yield*Time)) + Face*exp(-yield*Maturity);duration= sum( (C* Time.* exp(-yield*Time) )/ Price )+Fa